How to Read a Central Bank Meeting

A rate decision is the least interesting part of a central bank meeting. The market trades the guidance and the surprise. Here is what to watch and how the reaction works.

Central bank meetings are among the few scheduled events that can move a currency hard in seconds. What catches people out is that the headline rate decision is usually the least important part. The market has often priced the decision itself weeks in advance, and what it actually trades is the guidance and the surprise. Here is how I read one.

Why the meeting matters

A central bank sets the price of money, and the expected path of that price is one of the strongest forces in FX, as I covered in rate differentials explained. A meeting is where that path gets confirmed, revised or reset. So the meeting matters because of what it does to expectations of the future, far more than what it does today.

The three parts to watch

A modern meeting has three components, and each carries information.

The decision and statement. The rate move itself, plus the written statement that explains it. Because the decision is often widely expected, the more valuable part is usually the statement, and specifically what changed in it since the last meeting. A single altered phrase, a dropped commitment or a new concern can shift the whole outlook.

The projections. Many central banks publish updated economic forecasts, and some publish a set of individual rate expectations from their policymakers, often called the dot plot. These show where the committee thinks rates, growth and inflation are heading, and a shift in those projections since the previous round is a strong signal about the future path.

The press conference. The head of the central bank then takes questions, and the tone here can override everything that came before. A cautious statement paired with a confident, hawkish press conference tells a different story than the statement alone. The market listens closely to how the questions are answered, not only what the prepared text said.

Hawkish and dovish

Two words do most of the work in this world.

Hawkish describes a lean toward tighter policy, meaning higher rates or a slower path of cuts, usually to fight inflation. A hawkish surprise tends to support the currency, because it implies a better rate path.

Dovish describes a lean toward easier policy, meaning lower rates or a faster path of cuts, usually to support growth. A dovish surprise tends to weigh on the currency.

The important thing is that these labels apply to the whole message, not just the decision. You can have a hawkish cut, where the bank lowers rates but signals it will not do much more, and the currency rises. You can have a dovish hold, where the bank keeps rates steady but signals cuts are coming, and the currency falls. The decision and the guidance can point in opposite directions, and the guidance usually wins.

The reaction is about the surprise

Here is the part that ties it together. The currency does not react to the decision in isolation. It reacts to the gap between what the meeting delivered and what the market had already priced going in.

If a hike was fully expected and the bank delivers exactly that with no change in tone, the currency may barely move, or even fall as traders take profit on a priced-in event. If the bank holds but sounds far more hawkish than expected, the currency can jump despite no rate change at all. Before every meeting I try to have a clear sense of what the market is already expecting, because the reaction lives entirely in the distance between that expectation and the outcome.

How I read one

Going into a meeting, I fix in my mind what is priced, both the decision and the expected tone. Then I watch the three parts in order and ask a single question at each stage. Did this move the expected rate path higher or lower than what was already priced. The statement changes, the projections and the press conference each get measured against that baseline.

After the meeting, I fold the result back into the wider picture rather than trading the knee-jerk move on its own. A genuinely hawkish shift matters most when it lines up with the other reads, the positioning and the risk backdrop, which is the corroboration approach I described in how corroboration works.

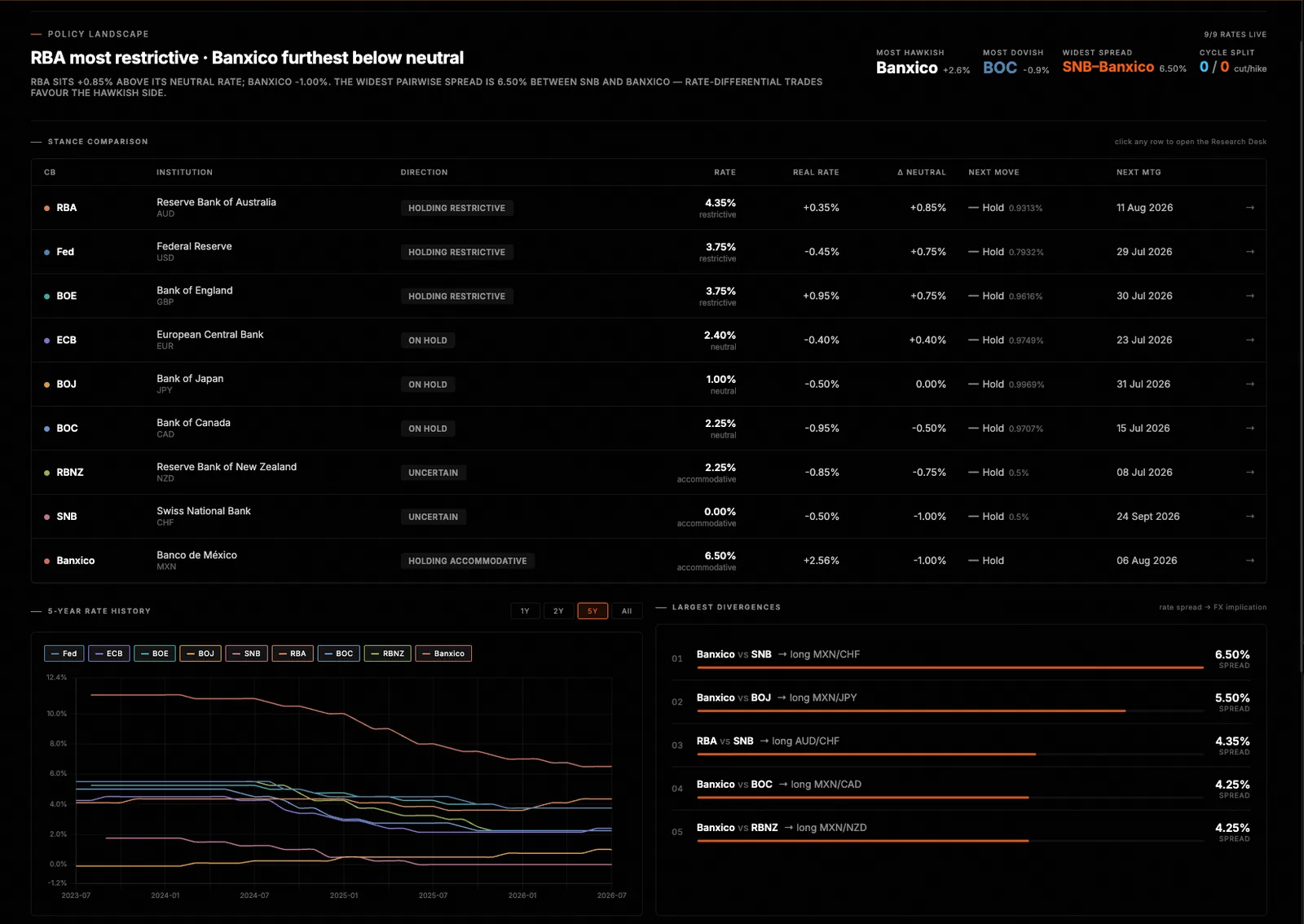

In WatchTower Terminal I keep the stance of each major central bank and the expected rate path in one view, so going into a meeting I can see clearly what is already priced and judge the outcome against it rather than against a blank page.

The decision is the headline. The guidance is the story. Trade the story.

Read the market the way this page describes.

WatchTower Terminal turns bank research, positioning and central-bank data into one clear read across FX, metals and global indices. Start free, no card required.