Rate Differentials Explained: Why Interest Rates Move Currencies

Interest rate differentials are one of the strongest forces in FX. Here is what they are, why the expected path matters more than the level, and when they stop working.

If I had to explain why one currency strengthens against another using a single idea, I would reach for the interest rate differential first. It is not the only driver, and it does not always win, but over the medium term it is one of the most reliable forces in the FX market. Here is how I think about it.

What a rate differential is

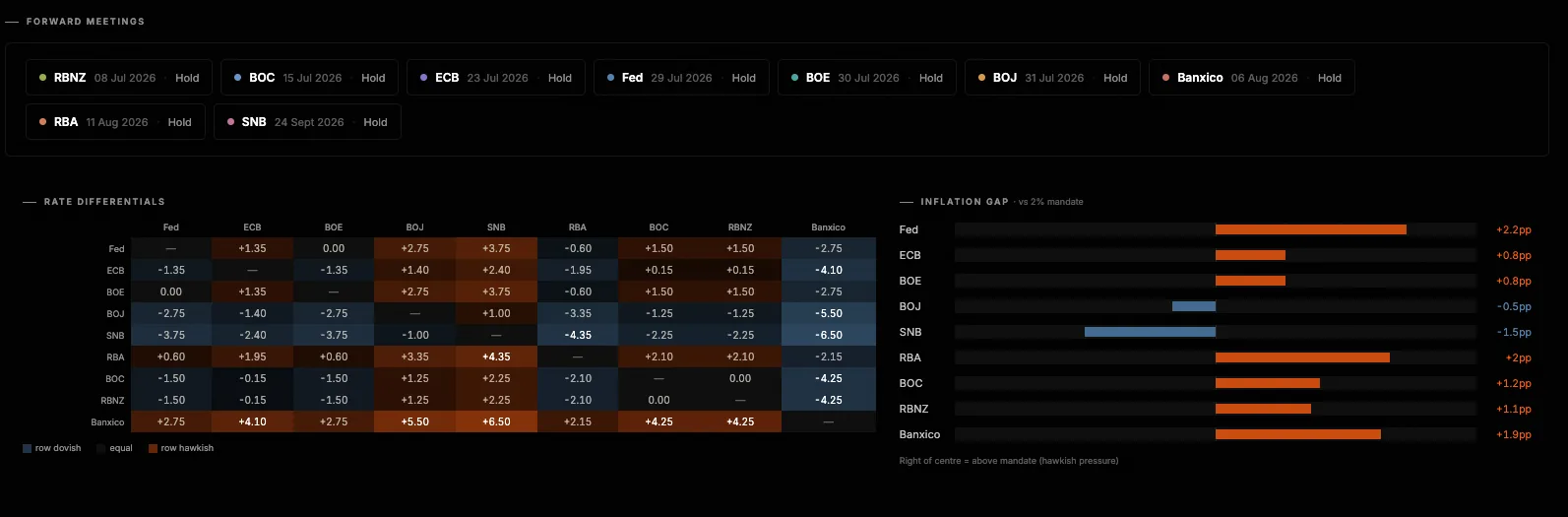

A rate differential is simply the gap between the interest rates of two currencies. If rates in one economy sit at 5% and the other at 1%, the differential is four percentage points in favour of the higher-yielding currency.

Capital is drawn to yield. All else equal, money flows toward the currency that pays more to hold it, and that flow tends to support its value. This is the mechanism behind the carry trade, where a trader borrows in a low-yielding currency and holds a higher-yielding one to earn the difference. When a lot of capital does this at once, it pushes the higher-yielder up and the funder down.

The level is the setup. The path is the trade.

Here is the part most people miss. The current differential is already known to everyone, and markets price known information almost immediately. What actually moves currencies is the change in the expected differential.

Currencies react to the direction of travel. If a central bank is expected to raise rates faster than markets previously thought, its currency tends to strengthen well before those hikes arrive, because traders are pricing the future path today. The reverse is just as true. A currency can weaken while its central bank is still cutting, simply because the market decided the cutting cycle would be shallower than feared.

So when I look at rates, I am really asking two questions. Where does the differential sit now, and, more importantly, how is the expected path shifting. A widening expected differential is a tailwind. A narrowing one is a headwind, regardless of where the absolute level sits today.

Watch real rates, not just nominal

The headline policy rate is the nominal rate. Subtract expected inflation and you get the real rate, which is what a global investor actually earns in purchasing-power terms.

A currency with a high nominal rate but even higher inflation can be deeply unattractive once you adjust for it. When I compare two currencies I try to keep real rates in view, because a nominal-rate story that falls apart on the real-rate view is a weak foundation for a trade.

The market’s favourite proxy

Traders often use the two-year government bond yield spread between two economies as a shorthand for the rate differential, because that part of the curve captures the market’s expectations for policy over the next couple of years. When the two-year spread moves in favour of a currency, that currency frequently follows. It is a clean, forward-looking read on the same idea, and it updates continuously rather than only on central-bank meeting days.

When rate differentials stop working

This is the honest part. Rate differentials are powerful, and they get overridden regularly.

The clearest override is risk sentiment. In a genuine risk-off episode, capital rushes toward safe-haven and funding currencies such as the dollar, the yen and the Swiss franc, even when their yields are unattractive. Carry trades unwind violently in exactly these moments, because the people holding them all reach for the exit at once. A currency can have every rate advantage and still fall hard in a panic.

The second override is that the differential is already priced. If a hiking cycle is fully expected, the currency may have already done its move, and the actual hikes can even trigger a sell-off as traders take profit. Buying a currency purely because it has a high rate, with no view on whether the path is still improving, is how people end up long at the top of a cycle.

How I use it

I treat the rate differential and its expected path as the backbone of a currency view, then I check it against everything else. Is research consensus leaning the same way. Is positioning already stretched in that direction. Is the broader risk environment supportive or hostile to carry. When the rate path and the corroborating evidence agree, I have a real thesis. When the rate story says one thing and risk sentiment says another, I know the trade is fragile and I size accordingly.

In WatchTower Terminal I keep the policy rates, the expected rate path and the differentials for each pair in one place, next to the central-bank stance and the macro score, so the direction of travel is obvious at a glance rather than something I have to assemble by hand.

Rate differentials are the current under the surface. Most of the time they carry the market in one direction. The job is knowing when a bigger wave, usually risk sentiment, is about to run the other way. For the sentiment side of that read, see the guide on reading the COT report.

Read the market the way this page describes.

WatchTower Terminal turns bank research, positioning and central-bank data into one clear read across FX, metals and global indices. Start free, no card required.