How to Read Bank Research Consensus in FX

Sell-side FX research is noisy and often wrong. Used well, the consensus across many banks is still a genuine edge. Here is how I read it, and how to avoid herding.

Every major bank runs an FX strategy desk, and every one of them publishes views on where currencies are heading. Read one in isolation and you learn almost nothing, because any single desk can be confident and wrong. Read the whole field together and a different, more useful picture appears. This is how I use bank research consensus without letting it herd me.

What sell-side FX research actually is

Banks publish research for their clients: the funds, corporates and institutions who trade through them. A typical note lays out a view on a currency, the reasoning behind it, and often a forecast for where the pair might trade over the coming quarters. The strategists writing them are well resourced and close to the flow, and they are also human, subject to the same anchoring and career incentives as anyone.

That is the key thing to hold in mind. A single bank’s call is one informed opinion. The value is not in any one voice. It is in seeing many of them at once.

Consensus is a base rate, not a prophecy

When I look across thirty banks and most of them lean bullish on a currency, that consensus is a base rate. It tells me where the weight of informed institutional opinion sits, and that is genuinely useful context. It is the starting point for a view, and it is the thing my own analysis has to either agree with or argue against.

What consensus is not is a prediction I should follow blindly. The crowd of banks can be wrong together, and it frequently is at turning points, because the same information and the same models push everyone toward the same conclusion at the same time. So I use consensus to answer one question first: what does the informed crowd already believe. Everything after that is about whether I agree, and why.

Disagreement is information

The reading I find most valuable is dispersion, meaning how much the banks disagree.

When almost every desk lines up on the same side, the view is crowded. That is worth knowing, because a crowded consensus leaves little room for pleasant surprises and a lot of room for a painful unwind if the story cracks. When the desks are split, with a meaningful group on each side, the market has a real debate on its hands, and the pair is more likely to be driven by the next data point that settles the argument.

Tight agreement and wide disagreement are two completely different environments, and they call for different caution. I always look at where consensus sits and how tightly it clusters, together.

Revisions matter more than levels

A forecast is a snapshot of what a desk believed on the day it was written. What tells me something is happening is when those views start to move.

If several banks revise their calls in the same direction over a short window, that shift in consensus is a signal in its own right, often a cleaner one than the level of the consensus itself. It means new information is being absorbed across the institutional world at once. I pay close attention to the direction consensus is travelling, because a consensus that is quietly turning is usually early to a change in the trend.

The honest limitations

I want to be straight about where this breaks down.

Short-term forecast accuracy across the industry is poor. Exchange rates are notoriously hard to predict over weeks and months, and the honest research desks will tell you the same. Treat point forecasts as a rough sense of direction and conviction, never as price targets to trade against mechanically.

Herding is real. Because desks read each other and share data, consensus can become a feedback loop that drifts away from reality until something forces a repricing. The moments consensus is most unanimous are often the moments it is most exposed.

And research reflects a house view that can lag fast-moving events. In a genuine shock, price will move long before the notes catch up.

How I use it

I read consensus as one of several corroborating layers, never as the answer. My process is to form a macro view from rates, policy and the data, then hold it up against the research crowd. When my thesis and the consensus agree, and positioning is not already stretched the same way, I have strong corroboration. When I disagree with a crowded consensus, I make sure I can articulate exactly why, because betting against the informed crowd demands a real reason, not a hunch.

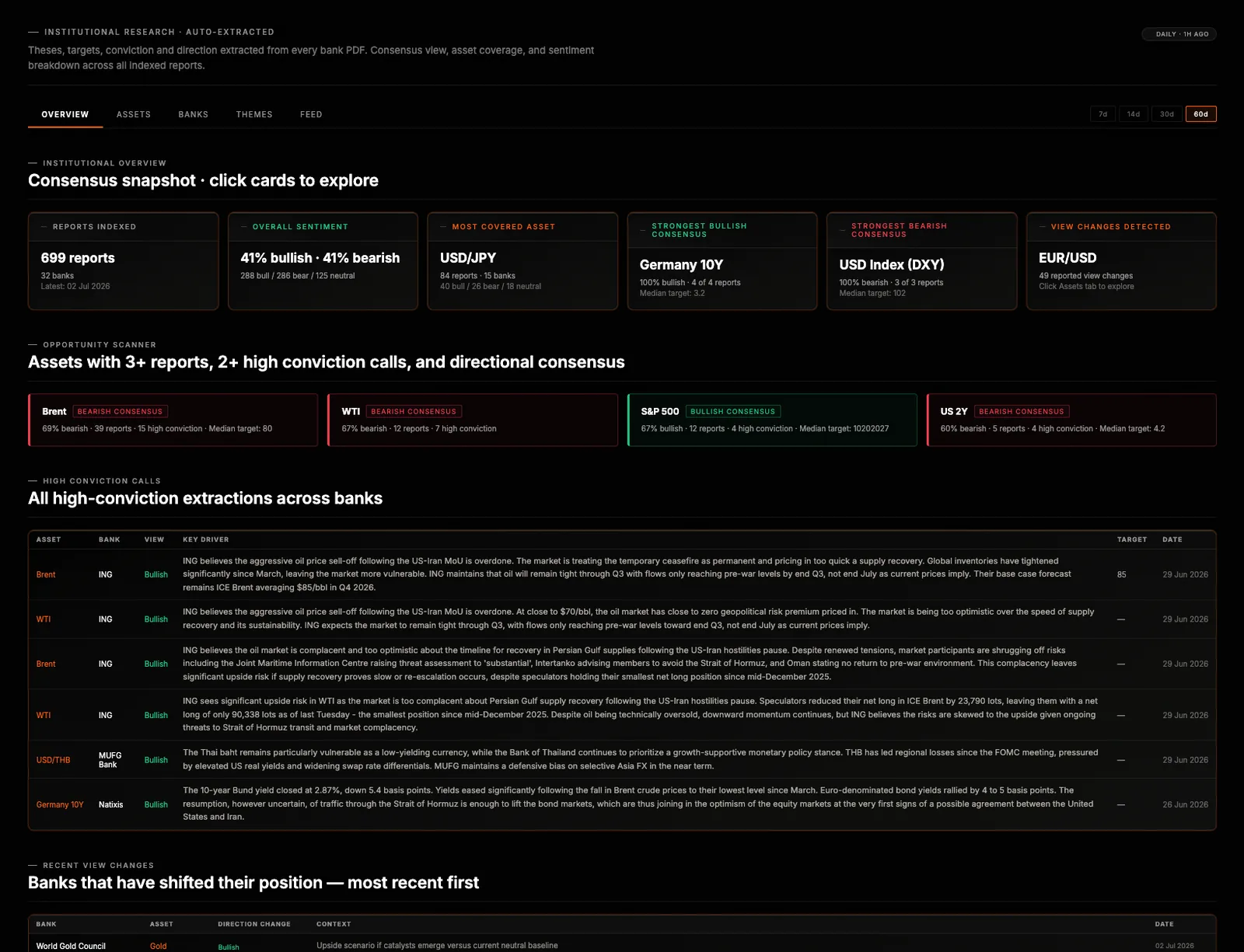

In WatchTower Terminal the consensus across more than thirty institutions sits next to positioning and the macro score for each asset, with the leaning and the spread of views in one read, so I can see agreement, disagreement and shifts without wading through thirty separate PDFs.

Bank research is a room full of informed opinions arguing with each other. The edge is in listening to the whole room, noticing when it goes quiet and unanimous, and knowing that is exactly when to think for yourself. For the positioning side of the same corroboration, see the guide on reading the COT report, and for the macro backbone, rate differentials explained.

Read the market the way this page describes.

WatchTower Terminal turns bank research, positioning and central-bank data into one clear read across FX, metals and global indices. Start free, no card required.